Have you ever wondered why you feel worse about losing $20 than you feel good about finding $20? Or why some customers stick with the same brand for years despite better options elsewhere? The answers lie in two powerful forces that shape our decisions every day: loss aversion and risk aversion.

These two psychological concepts might sound similar, but they drive very different customer behaviors. Understanding them can be the difference between a marketing campaign that flops and one that drives significant sales growth. Whether you’re a business owner, marketer, or simply curious about why we make the choices we do, this article will give you practical insights you can use right away.

By the time you finish reading, you’ll understand:

- How loss aversion makes customers 2x more sensitive to losses than equivalent gains

- Why risk-averse customers might pay more for certainty

- Practical marketing strategies that leverage these behaviors

- Ethical ways to apply these insights without manipulating customers

Ready to unlock the psychology that drives customer decisions? Let’s dive in!

Theoretical Foundations: The Science Behind Our Choices

Before we explore how these biases affect customer behavior, let’s build a solid understanding of where these concepts come from and what they actually mean. This foundation will help you better grasp why customers behave the way they do when making decisions.

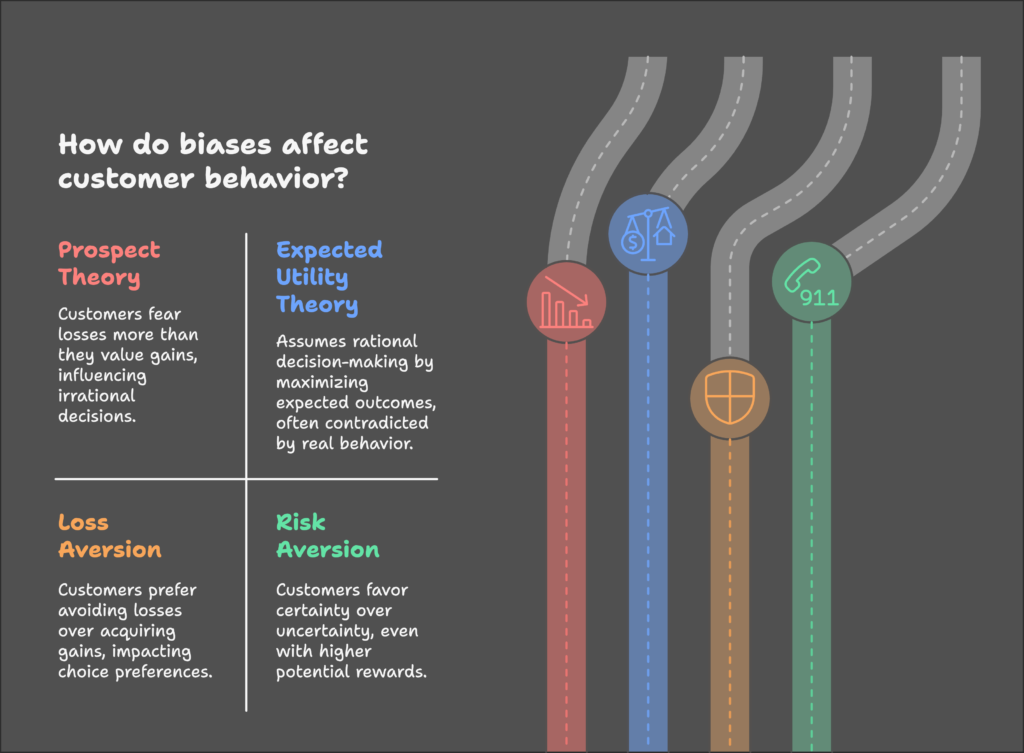

Prospect Theory: Not All Outcomes Are Created Equal

In the 1970s, psychologists Daniel Kahneman and Amos Tversky discovered something fascinating about human decision-making: we don’t evaluate gains and losses equally. Their groundbreaking “Prospect Theory” revealed that people feel the pain of losses roughly twice as strongly as they feel the pleasure of equivalent gains.

This asymmetry explains many seemingly irrational decisions. For instance, why would someone refuse a bet with a 50% chance to win $120 and a 50% chance to lose $100? Mathematically, this is a good deal (expected value of +$10), but emotionally, the fear of losing $100 outweighs the excitement of potentially winning $120.

Expected Utility Theory: The Traditional View

Before Prospect Theory, economists relied on Expected Utility Theory, which assumed people make rational decisions by maximizing their expected outcomes. This theory suggested people would always take a bet if the mathematical expected value was positive.

But real life shows this isn’t how we actually behave. People regularly choose smaller, guaranteed rewards over larger, uncertain ones—even when the math suggests they shouldn’t. This gap between theoretical rationality and actual behavior is where loss aversion and risk aversion come into play.

Key Definitions: Similar But Different

Let’s clarify what these terms actually mean:

- Loss Aversion: The tendency to prefer avoiding losses over acquiring equivalent gains. It’s an emotional bias where losses hurt more than gains feel good.

- Risk Aversion: The preference for certainty over uncertainty, even when the uncertain option has a higher expected value. It’s about avoiding the unknown, not just losses.

Now that we understand their origins, let’s explore how these two concepts differ and why that matters for customer behavior. Are you ready to see how our brains actually make decisions rather than how economists think we should? Let’s continue!

Key Differences Between Loss Aversion and Risk Aversion

Though they’re often confused, loss aversion and risk aversion operate through different psychological mechanisms and lead to different behaviors.

In this section, we’ll explore what makes them distinct and how they affect decision-making in unique ways.

Psychological Mechanisms: Different Mental Drivers

Loss aversion and risk aversion stem from different parts of our decision-making process:

- Risk Aversion is rooted in our discomfort with uncertainty. It’s why many people prefer a guaranteed $50 over a 50% chance to win $120 (even though the second option has a higher expected value of $60). This behavior isn’t about fearing loss specifically—it’s about preferring the known over the unknown.

- Loss Aversion, on the other hand, is about the emotional pain of losing what we already have. It’s why investors hold onto losing stocks too long—selling would mean accepting the loss, which hurts more than the potential gain from reinvesting elsewhere.

Behavioral Manifestations: How They Look in Action

These different mechanisms lead to distinctly different behaviors:

- A risk-averse person typically avoids gambles altogether, preferring guaranteed outcomes even if they’re smaller. They might choose fixed-rate mortgages over adjustable ones, or bonds over stocks.

- A loss-averse person, however, can become surprisingly risk-seeking when facing potential losses. They might double-down on bad investments or chase losses in gambling—behaviors that actually increase risk but aim to avoid confirming a loss.

This distinction explains why the same person might be extremely cautious in some situations but take big risks in others.

Neuroeconomic Insights: What’s Happening in the Brain

Modern brain imaging studies have revealed fascinating differences in how our brains process these scenarios:

- When facing potential losses, the brain’s amygdala (associated with emotional responses) shows increased activity, triggering a stronger emotional reaction.

- When assessing risk, the prefrontal cortex (responsible for logical reasoning) plays a more prominent role.

- Hormones like dopamine (rewards) and cortisol (stress) influence these processes, explaining why emotions often override logical calculations in decision-making.

This scientific understanding helps explain why customers don’t always behave “rationally” according to traditional economic models. But how exactly do these biases show up in everyday customer behavior? That’s what we’ll explore next…

Impact on Customer Behavior

Now that we understand the theoretical differences, let’s look at how loss aversion and risk aversion actually influence real-world customer decisions. These concepts aren’t just academic theories—they shape purchasing decisions, brand loyalty, and responses to marketing every single day.

Financial Decision-Making: Money Matters

Financial choices highlight the distinct impacts of these biases:

- Loss Aversion drives the “disposition effect” where investors quickly sell winning stocks (to lock in gains) but hold onto losing investments far too long (to avoid confirming losses). This tendency explains why many individual investors underperform the market.

- Risk Aversion explains why many people keep large amounts in low-interest savings accounts rather than investing in higher-return options like index funds. The certainty of having that money “safe” outweighs the mathematical advantage of investing, even over long time horizons.

Purchasing Behavior: Everyday Choices

These biases affect all kinds of shopping decisions:

- Loss Aversion explains why customers readily purchase extended warranties for products (even when mathematically overpriced). The fear of a future loss (repair costs) outweighs the immediate loss of paying for warranty protection.

- Risk Aversion contributes to strong brand loyalty. Customers often stick with familiar brands even when cheaper or potentially better alternatives exist. The certainty of getting what they expect reduces the perceived risk of disappointment.

Marketing and Messaging: Crafting Effective Communications

Smart marketers already leverage these biases (sometimes without even realizing it):

- Loss-Framed Messages like “Don’t miss out!” or “Last chance!” create urgency by triggering loss aversion. They work because the fear of missing an opportunity feels worse than the pleasure of gaining something new.

- Risk-Reducing Messages like “30-day money-back guarantee” or “Free returns” address risk aversion by removing uncertainty from purchasing decisions. This is why free trials are so effective—they eliminate the risk of making the wrong choice.

Understanding these patterns isn’t just theoretical—it gives us practical insight into how real customers make decisions. But how do these biases play out during major events like economic crises? And what specific tactics can businesses use to ethically leverage these insights? Let’s look at some fascinating real-world examples…

Case Studies: Real-World Examples

Theory is helpful, but seeing these biases in action makes them much more tangible. In this section, we’ll explore specific examples that demonstrate how loss aversion and risk aversion drive behavior in various contexts. These case studies will help you recognize these patterns in your own business environment.

Investment Decisions During COVID-19

The COVID-19 pandemic created a natural experiment in how these biases function during crisis:

- Loss Aversion Spike: In March 2020, stock markets plummeted as panic selling accelerated. Many investors who had previously followed “buy and hold” strategies suddenly sold at market bottoms—not because it was rational, but because the emotional pain of watching their portfolio value drop became unbearable.

- Risk Aversion Response: Simultaneously, many investors moved money to gold, government bonds, and cash—accepting significantly lower returns for the security of stable assets. This wasn’t about avoiding losses specifically but seeking certainty in uncertain times.

The pandemic showed how these biases intensify during periods of heightened stress and uncertainty.

Consumer Responses to Scarcity

Scarcity (real or perceived) triggers both biases in fascinating ways:

- Loss Aversion and Limited-Time Offers: When Black Friday deals say “Today Only,” they create artificial scarcity that triggers loss aversion. Customers fear missing out on savings, which feels like a loss, driving immediate purchasing decisions.

- Risk Aversion and Subscription Models: The growing popularity of subscription services for everything from software to meal kits stems partly from risk aversion. Customers prefer the predictable spending of subscriptions to the uncertainty of one-time purchases that might not deliver as expected.

Behavioral Pitfalls: Common Traps

These biases can lead to problematic behavior patterns for both customers and businesses:

- Overconfidence Combined with Loss Aversion: Day traders often believe they can “beat the market” (overconfidence) while simultaneously refusing to sell losing positions (loss aversion). This combination leads to portfolio underperformance and potential financial harm.

- Anchoring and Herding: Risk-averse customers often rely on reference points (“anchors”) like original prices or follow crowd behavior (“herding”) to reduce perceived risk. This explains why online reviews and “bestseller” labels significantly impact purchasing decisions.

These real-world examples show how powerful these psychological forces are in shaping behavior. But as a business owner or marketer, how can you ethically apply these insights to improve your marketing and customer relationships? Let’s explore effective strategies next…

Strategies for Businesses

Now comes the practical part: how can businesses ethically leverage these psychological insights to improve marketing, increase conversions, and build stronger customer relationships? In this section, you’ll discover specific tactics you can implement right away, all based on our understanding of loss aversion and risk aversion.

Leveraging Loss Aversion

Here are strategies that tap into customers’ stronger response to potential losses:

- Frame Benefits as Loss Prevention: Instead of saying “Our home security system gives you peace of mind,” try “Don’t leave your family’s safety to chance.” The second approach frames the benefit as avoiding a loss rather than gaining something.

- Use Scarcity Tactics Authentically: Highlight genuine limitations like “Only 5 spots left in our March workshop” or “Limited edition—once they’re gone, they’re gone.” But remember: artificial scarcity can damage trust if customers perceive manipulation.

- Offer Trial Periods: Free trials work because after using a product, customers feel ownership—and giving it up feels like a loss. This is why Netflix and other services offer free trials; once you’ve experienced the service, canceling feels like losing something you already have.

Addressing Risk Aversion

These tactics help reduce the uncertainty that triggers risk aversion:

- Provide Strong Guarantees: Money-back promises, free returns, and satisfaction guarantees all reduce the risk of making a “wrong” choice. This is especially important for high-value purchases or when customers can’t physically examine products (like online shopping).

- Show Social Proof: Customer testimonials, case studies, and reviews help risk-averse customers feel safer about their decisions. When they see others have had positive experiences, the perceived risk decreases.

- Offer Detailed Information: Comprehensive product details, comparison charts, and educational content all help reduce uncertainty. The more customers understand what they’re getting, the less risky the purchase feels.

Balancing Both Biases

The most effective approaches often address both biases simultaneously:

- Create Hybrid Messaging: Combine both perspectives in your marketing. For example, “Secure your retirement future (addressing risk aversion) while avoiding costly market mistakes (addressing loss aversion).”

- Develop Personalized Approaches: Different customer segments may lean more toward one bias than the other. Segment your audience and tailor messages accordingly—more conservative customers might respond better to risk-reduction messaging, while others might be more motivated by loss-prevention framing.

- Test Different Frameworks: A/B test different message framing to see which resonates more with your specific audience. The results might surprise you and will provide valuable insights about your customer base.

These strategies can significantly improve marketing effectiveness, but they also raise important ethical questions. How can we use these insights responsibly without crossing into manipulation? That’s what we’ll explore next…

Ethical Considerations

With great psychological insight comes great responsibility. While understanding loss aversion and risk aversion can make marketing more effective, it’s essential to consider the ethical implications. This section explores how to apply these concepts responsibly while building authentic customer relationships.

Manipulation vs. Empowerment

There’s a crucial line between leveraging natural psychology and manipulating customers:

- Avoid Fear-Based Exploitation: Generating unnecessary anxiety to drive sales (like vastly exaggerating risks) might boost short-term conversions but damages long-term trust. Instead, address genuine concerns with honest solutions.

- Focus on Customer Outcomes: Ask whether your marketing helps customers make better decisions for their actual needs. If you’re simply triggering bias-based responses to sell products that don’t deliver real value, you’re on ethically shaky ground.

- Promote Informed Choices: Clear communication, transparent pricing, and easy-to-understand terms help customers make decisions aligned with their true preferences rather than just responding to psychological triggers.

Cultural and Demographic Nuances

Loss aversion and risk aversion don’t affect everyone equally:

- Cultural Differences: Research suggests collectivist cultures (like many East Asian societies) may exhibit different patterns of loss and risk aversion compared to more individualist Western cultures. Marketing that works in one region might not translate effectively to another.

- Generational Variations: Different generations show varying levels of risk tolerance. Gen Z consumers often demonstrate more comfort with uncertainty in technology adoption, while Baby Boomers may show stronger loss aversion regarding retirement savings.

- Individual Differences: Even within demographic groups, personal experiences and personality traits create significant variation in how strongly these biases operate. Avoid one-size-fits-all assumptions.

Understanding these ethical considerations helps create marketing that respects customers while still being effective. But what does the future hold for our understanding of these biases? Let’s look at emerging trends and research that could transform how we view customer psychology…

Future Directions

The fields of behavioral economics and consumer psychology continue to evolve rapidly. This section explores emerging trends and research directions that could shape how businesses understand and apply concepts like loss aversion and risk aversion in the coming years.

Technological Innovations

New technologies are transforming how we understand and respond to customer psychology:

- AI-Driven Behavioral Insights: Machine learning algorithms are increasingly able to identify individual customer tendencies toward loss or risk aversion based on browsing and purchasing patterns. This allows for highly personalized marketing that addresses each customer’s specific psychological profile.

- Gamification Approaches: Companies are developing sophisticated ways to reframe risks and rewards through game-like elements. Loyalty programs that turn spending into “points” and create achievement levels can help overcome loss aversion by making the experience feel more like gaining (points, status) than spending (money).

- Virtual Reality Testing: VR environments allow companies to test customer responses to different framings and scenarios without real-world consequences. This provides richer data on how these biases operate in realistic settings.

Research Opportunities

Several promising research directions could deepen our understanding:

- Post-Pandemic Behavioral Shifts: Researchers are conducting longitudinal studies to determine whether the COVID-19 pandemic created lasting changes in risk and loss attitudes. Early evidence suggests some people became more risk-averse, while others developed a “life is short” mentality that decreased risk aversion.

- Cross-Disciplinary Approaches: The integration of neuroscience, psychology, and economics is revealing how biological factors (stress hormones, brain structure) interact with psychological biases. This could lead to more nuanced models of customer decision-making.

- Contextual Variations: Growing research explores how environmental factors and situational contexts influence the strength of these biases. For example, time pressure appears to intensify loss aversion, while certain social settings can mitigate risk aversion.

These developments suggest we’re moving toward increasingly sophisticated and personalized approaches to understanding customer psychology. But what does all this mean for your business right now? Let’s wrap up with key takeaways and actionable recommendations…

Conclusion

We’ve covered a lot of ground in our exploration of loss aversion and risk aversion. Let’s bring it all together with key insights and practical recommendations you can apply to your business today.

Summary of Key Insights

- Loss aversion and risk aversion are distinct psychological forces that influence customer decisions in different ways.

- Loss aversion makes people approximately twice as sensitive to losses as to equivalent gains, while risk aversion drives preference for certainty over uncertain outcomes.

- These biases affect everything from purchasing decisions and brand loyalty to investment choices and responses to marketing messages.

- Ethical application of these concepts can improve marketing effectiveness while respecting customer autonomy.

- Cultural, generational, and individual factors create significant variation in how strongly these biases operate.

Final Recommendations

Here are actionable steps to apply these insights effectively:

- Audit Your Current Marketing: Review your existing messaging to identify whether you’re primarily addressing loss aversion, risk aversion, or neither. Look for opportunities to incorporate both types of framing.

- Test Different Approaches: Implement A/B testing to determine which framing resonates more with your specific audience. Don’t assume—get actual data on what works.

- Segment Your Strategy: Different customer segments may respond differently to loss-framed versus risk-reducing messages. Develop tailored approaches for key customer groups.

- Balance Short and Long-Term: While triggering loss aversion can boost immediate conversions, building trust through risk reduction often yields better long-term customer relationships.

- Stay Ethical: Remember that the goal is to help customers make choices aligned with their actual needs, not to manipulate them into purchases they’ll regret.

By understanding and ethically applying insights from behavioral economics, you can create more effective marketing that resonates with how customers actually make decisions—not how traditional economic theory says they should.

Remember: If you run a Shopify store and want to apply these insights to grow your business, the Growth Suite application offers tools to implement many of these strategies automatically, helping you increase conversions while building stronger customer relationships.

References

- Hamelin & Harcar (2020): Neuroscience of Loss Aversion. Link

- Investopedia (2024): Prospect Theory. Link

- InsideBE (2022): Loss Aversion Mechanisms. Link

- Semantic Scholar (2023): Trusting Behavior and Risk Preferences. Link

- The Decision Lab (2021): Prospect Theory. Link

- Wikipedia (2024): Loss Aversion. Link

- Semantic Scholar (2023): COVID-19 Investment Behavior. Link